OVERVIEW

What is Premium Financing?

Premium financing is a strategy that allows high-net-worth individuals to leverage third-party loans to pay life insurance premiums. This approach helps preserve capital for other investments while maintaining comprehensive life insurance coverage.

Borrow funds to pay premiums instead of using personal assets

Maintain capital available for investment opportunities

Avoid forced liquidation of existing investments

Create substantial death benefits for estate tax payments

The Premium Finance Advantage

Why Choose Premium Financing?

Premium financing offers unique advantages for wealth preservation and growth.

Leverage Your Wealth

Borrow funds to pay premiums instead of using personal assets. Maintain capital available for investment opportunities.

Cash Flow Optimization

Preserve liquid funds for other personal or investment uses. Prevent tax consequences from selling assets prematurely.

Estate Planning Benefits

Create substantial death benefits for estate tax payments. Enable significant wealth transfer to heirs.

Family Protection

Large death benefit provides family security. Efficient wealth transfer preserves inheritance.

HOW IT WORKS

The Premium Financing Process

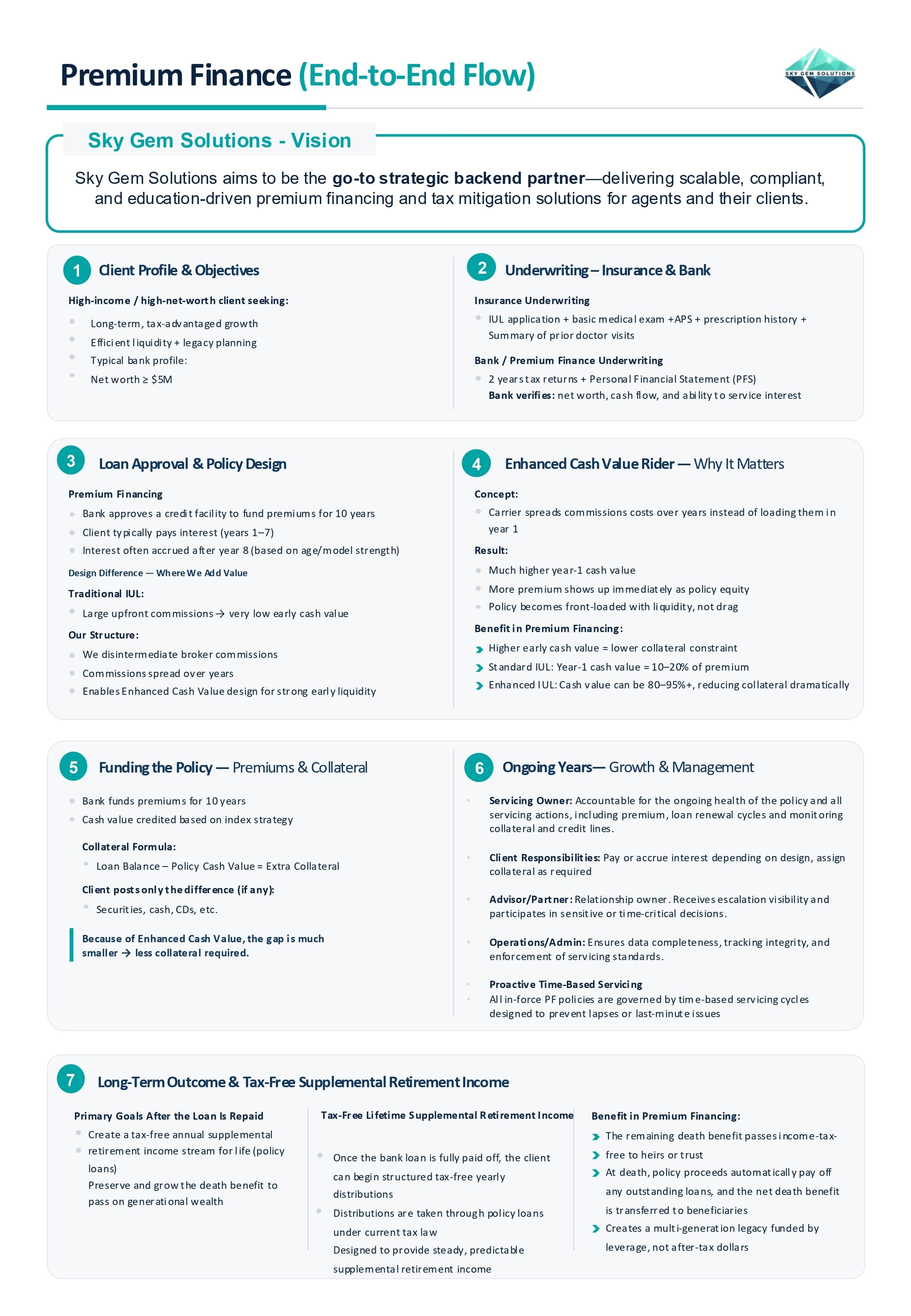

A premium finance life insurance policy works by allowing a high-net-worth individual to borrow funds from a third-party lender to pay the premiums on a large permanent life insurance policy, rather than paying the premiums out of their own assets. Here's a more detailed explanation:

01

Applying for a High-Value Life Insurance Policy

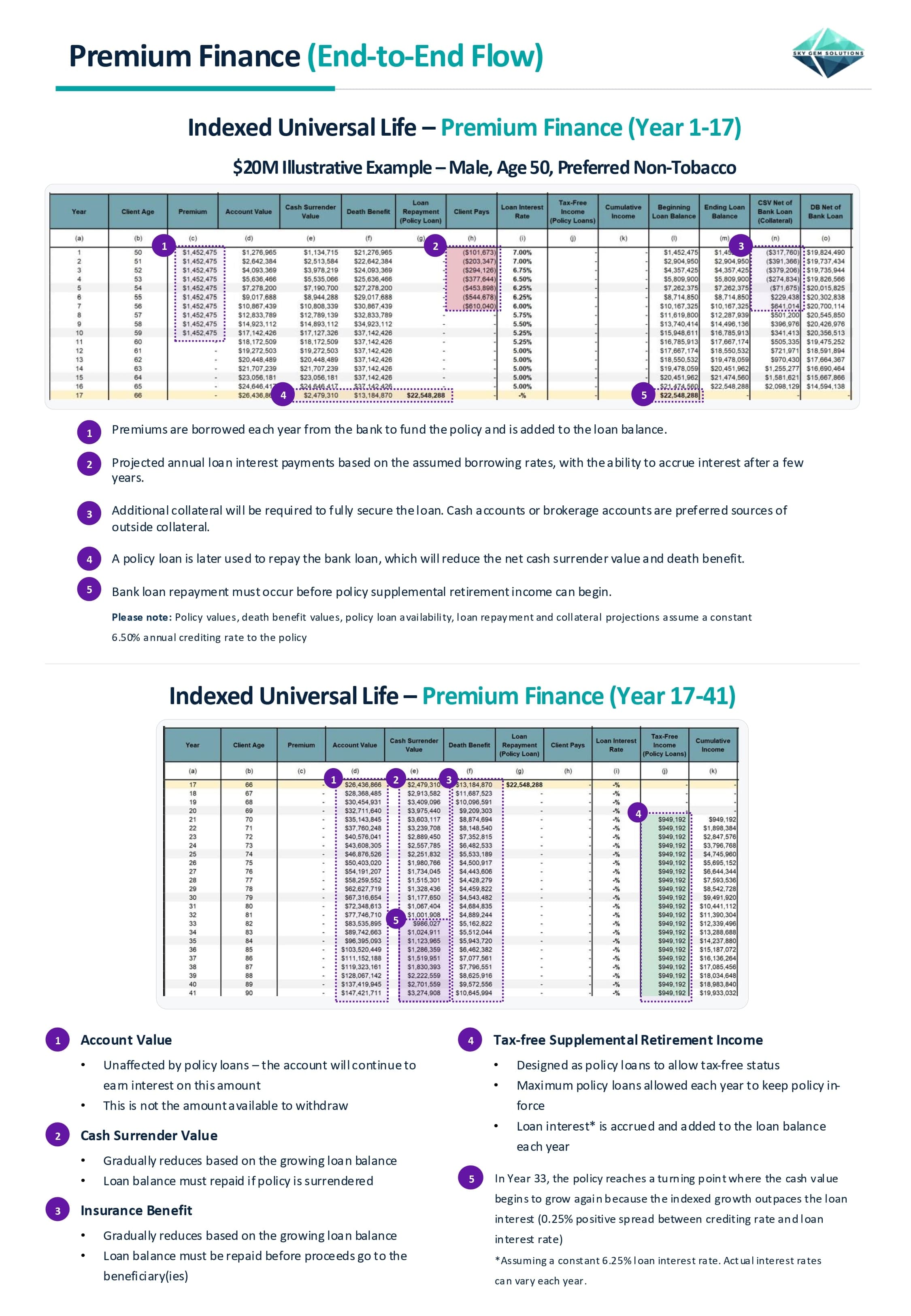

The policyholder applies for a substantial permanent life insurance policy, often with a death benefit in the millions or tens of millions of dollars. Common policy types used are indexed universal life (IUL) or whole life insurance.

02

Financing Premiums Through a Lender

Instead of paying the large premiums out-of-pocket, the policyholder obtains a loan from a premium finance lender to cover some or all of the premiums.

03

Assigning the Policy and Additional Collateral

The lender requires the life insurance policy itself to be assigned as collateral for the loan. Additional collateral like securities, real estate or business interests may also be required, especially in the early policy years before substantial cash value has accumulated.

04

Making Loan Payments to the Lender

The policyholder makes regular loan payments to the lender, typically interest-only payments initially. Some may choose to capitalize the interest by adding it to the loan balance.

05

Leveraging Cash Value Growth to Repay the Loan

The goal is for the cash value growth inside the life insurance policy to eventually equal or exceed the compounding loan balance from the premium financing. This allows the policy's values to effectively "repay" the loan over time.

06

Accessing Benefits: Cash Value or Death Benefit

The policyholder can then access the policy's cash value through tax-free loans or withdrawals for supplemental retirement income. Or they can allow the policy to pay out the full tax-free death benefit to their beneficiaries upon their passing.

COMPARISON

Premium Financing vs Traditional Life Insurance

Traditional

Premium Financing

Funding

Direct out-of-pocket payment

Third-party loan covers premiums

Policy Size

Smaller coverage amounts

Millions to tens of millions

Leverage

Limited to personal funds

Obtain larger coverage via borrowing

Cash Flow

Impacts liquid reserves

Preserves capital for investments

Interest Costs

No financing costs

Additional loan interest expense

Exit Strategy

Ongoing premium payments

Repay using cash value or death benefit

Enhanced Cash Value Structure

Our enhanced cash value approach provides significant advantages over traditional IUL structures.

i

Standard IUL: Year-1 cash value = 10-20% of premium. Enhanced IUL: Cash value can be 80-95%+, reducing collateral dramatically.

Traditional IUL Issues

-

Higher premiums compared to Term Life insurance

-

Low early cash value

-

High outside collateral required

-

Inefficient IRR

Our Enhanced Structure

Minimal front-loaded commissions

Commissions spread 5-7 years

High early cash value = lower collateral

Larger long-term cash value

Higher tax-free income potential

Bigger death benefit for same client outlay

IS IT RIGHT FOR YOU?

Ideal Client Profile

Premium financing is designed for high-income and high-net-worth individuals seeking specific financial goals.

Requirements

Net worth of $5M or more

Seeking long-term, tax-advantaged growth

Interest in efficient liquidity and legacy planning

Ability to service interest payments

Strong credit profile for bank approval

Financial Objectives

Create substantial death benefit

Preserve capital for other investments

Create substantial death benefit for estate planning

Generate tax-free supplemental retirement income

Build multi-generational wealth

Optimize estate tax planning

Learn

Premium Finance

End-to-End Flow

Download or view our comprehensive premium financing overview document.